Jack in the Box Bankruptcy Risk: Updated Analysis Incorporating Recent Shocks

Jack in the Box Inc. (NASDAQ: JACK), the quick-service restaurant chain behind its namesake brand and formerly Del Taco, continues to face intensifying pressures in a challenging fast-food sector. As of Q3 fiscal 2025 (ended July 6, 2025), core issues like declining same-store sales (-7.1%), planned closures (150–200 stores), and elevated debt persist amid the $115 million Del Taco sale (announced October 16, 2025, closing January 2026). Now, additional shocks—California’s AB1228 wage hikes, the Ozempic boom, SNAP benefit reductions, ICE raids, and recessionary signals—amplify vulnerabilities, particularly given 43% of JACK’s 2,200 stores in California. These factors threaten further revenue erosion and margin compression, pushing bankruptcy risks higher.

This updated analysis integrates these shocks into prior insights. Short-term liquidity ($38M cash, $96.5M revolver) holds, but sustained hits could trigger covenant breaches or refinancing failures.

Financial Snapshot Amid Shocks

Revenue and EBITDA trends worsen with labor inflation from AB1228 ($20/hr in 2024, $21/hr in 2025, plus 3.5% annual hikes), which spiked JACK’s labor costs 200 basis points year-over-year. Ozempic/semaglutide adoption drives reduced dining out (70%of users cooking more at home) and aversion to “unhealthy” fast food, potentially shaving 5–10% off traffic for calorie-dense chains like JACK. SNAP cuts (half benefits for November 2025 due to shutdown delays) hit low-income urban customers, including 1M+ in LA County, where JACK accepts EBT. ICE enforcement in CA correlates with 3.1% labor participation drops and reduced spending by Latino communities (key JACK demographic). Recession indicators—plummeting optimism (43.9 index), slowing GDP (1.6% projected 2025)—favor K-shaped dynamics, squeezing JACK’s value-sensitive base.

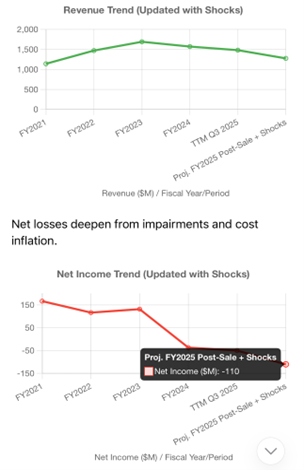

Post-sale projections now factor additional 3–5% SSS drag from these shocks, trimming EBITDA to $240–250M.

Revenue and Profit Trends

Shocks compound SSS weakness: Ozempic suppresses “food noise,” SNAP/ICE reduce disposable income for core customers, and recession prompts home cooking. AB1228 forces price hikes (offsetting only partially), risking further traffic loss.

Net losses deepen from impairments and cost inflation.

Debt and Leverage Pressures

$3.1B obligations unchanged by shocks, but EBITDA erosion drops coverage to 2.0–2.5x. Del Taco proceeds ($90–100M net) offer scant buffer against $200–300MFY2026 maturities.

Heightened Bankruptcy Pathways

Shocks elevate odds to 60%+ within 24 months, accelerating liquidity crunches.

- Failed 2026 Refinancing (Extreme High): Wage hikes and sales drops push leverage >6x; lenders demand premiums amid recession signals.

- Sales/FCF Collapse (Very High): Ozempic/SNAP/ICE combo could cut traffic 10–15%+ in CA-heavy ops; negative FCF $100M+ annually.

- Covenant/Operational Breaches (High): AB1228’s ongoing costs (statewide 18k jobs lost) strain royalties/franchisees.

- Macro Amplification (High): K-shaped recession hits JACK’s base hardest, with SNAP delays as near-term catalyst.

Mitigants and Outlook

“JACK on Track” refranchising and reimages offer hope for 5% SSS recovery, but shocks delay benefits. Shares $16, down 60% YTD. Monitor Q4 earnings (December 2025) and SNAP/ICE developments. JACK’s “zombie” status intensifies—restructuring favored for 50–70% creditor recovery.

Related posts

You may also find these articles interesting